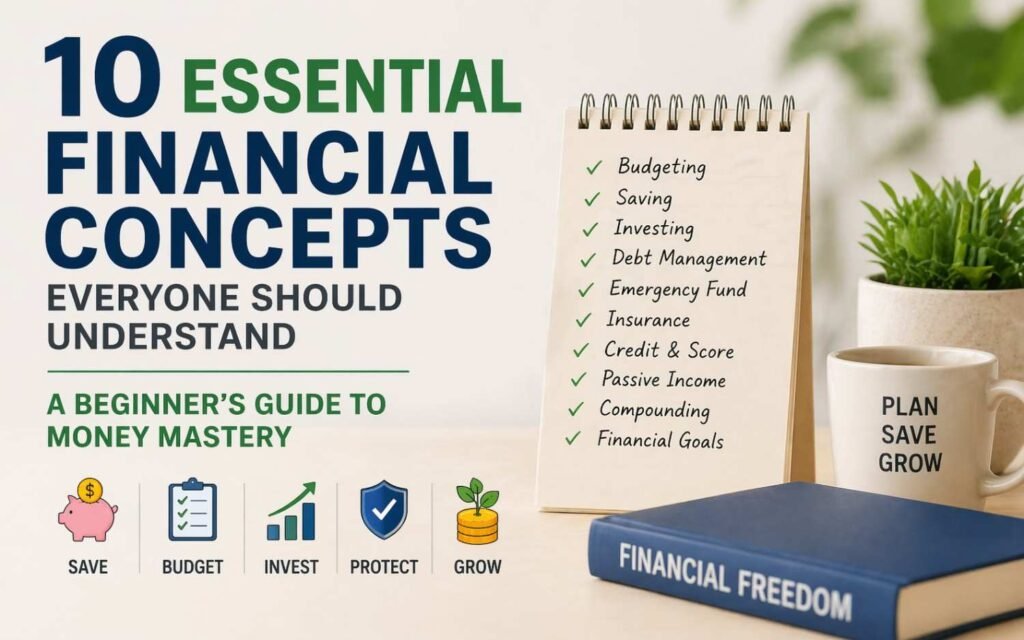

In a world where money touches every part of life—from your paycheck to your retirement plans—financial literacy isn’t optional; it’s empowering. The popular YouTube video Explaining Basic Financial Concepts YOU Should Understand by EverythingProfessor breaks down these fundamentals in a simple, relatable, and often humorous way. Whether you’re just starting your career or looking to level up your money game, these 10 core concepts will help you make smarter decisions, avoid common pitfalls, and build real wealth over time.

1. Taxes: The Price of Civilization

Picture this: You’ve just finished a tough month at work, check your bank account on payday, and—surprise—the number is noticeably smaller than your gross pay. That’s taxes at work.

Taxes are mandatory contributions that fund the “cost of civilization”—roads, schools, police, military, and public services. Common types include:

- Income tax (on what you earn)

- Sales tax (on purchases)

- Capital gains tax (on investment profits)

- Social Security (a forced retirement savings plan)

- Medicare (healthcare support for seniors and those with serious conditions)

The government already knows roughly what you owe, yet you still have to file and estimate it yourself. Some people pay quarterly, others annually. Fun fact: Countries with higher taxes often deliver better public services and higher quality of life. Understanding taxes helps you plan ahead, claim deductions legally, and avoid surprises.

2. Banks: More Than Just a Safe

Banks aren’t just fancy vaults for your cash. They act as financial middlemen through fractional reserve banking: they keep only a small portion of deposits on hand and lend out the rest.

They profit by charging borrowers higher interest rates than they pay savers. You get convenience (ATMs, apps, checks), earn a little interest on deposits, and enjoy safety—thanks to FDIC insurance that protects up to $250,000 per depositor if the bank fails.

3. Interest: The Double-Edged Sword of Money

Interest is simply the cost of borrowing money—or the reward for lending it.

- Borrow (loans, credit cards)? You pay interest.

- Save or invest? You earn it.

There are two main types: simple interest (straightforward) and compound interest (the real game-changer—it grows exponentially on itself). Missing credit card payments at 20%+ can balloon debt fast, while consistent investing at 7% can turn modest savings into serious wealth over decades.

Pro tip: Pay off high-interest debt aggressively and let your investments compound. Time is your biggest ally here.

4. Inflation: The Silent Thief of Purchasing Power

Inflation means your money slowly buys less over time. That $5 coffee today might cost $6 or $7 in a few years.

Causes include too much money chasing too few goods, supply chain problems, or rising consumer expectations. Governments target mild inflation (around 2%) as healthy and fight spikes by raising interest rates to slow spending and borrowing.

The takeaway? Cash sitting idle loses value. Your money needs to grow faster than inflation just to stay even.

5. Recessions: When the Economy Takes a Breather (or a Hit)

A recession is officially two or more consecutive quarters of economic decline. It brings layoffs, reduced spending, and business struggles.

Triggers can include high interest rates, global crises (wars, pandemics), or natural boom-and-bust cycles. Governments fight back with lower rates or stimulus checks to encourage spending.

Recessions feel painful but often act as necessary economic resets. Building an emergency fund and keeping debt low prepares you to weather them.

6. Credit Scores: Your Financial Reputation in a Number

Your credit score (ranging from 300–850) is a three-digit snapshot of how trustworthy you are as a borrower. Lenders use it to decide loan approvals and interest rates.

It’s calculated from five key factors:

- Payment history (biggest factor)

- Credit utilization (how much of your available credit you’re using)

- Length of credit history

- Credit mix (variety of accounts)

- New credit inquiries

Pay bills on time, keep balances low, and avoid opening too many new accounts. Scores above 750 unlock the best rates; low scores can make everything more expensive. Even having no debt can hurt your score if you have zero credit history.

7. Currency: It’s All About Trust

Money (currency) has no real intrinsic value—it’s a social construct based on collective belief and trust in the government that issues it.

Governments print it; central banks regulate the supply. Print too much → inflation. Print too little → economic slowdown. Think of Bitcoin or even a historical “stick” used as currency: its value exists only because we all agree it does.

8. Investing: Making Your Money Work for You

Investing is how you beat inflation and build wealth. Instead of trading time for money (a job), you trade money for the potential of more money in the future.

Popular options:

- Stocks → ownership in companies

- Bonds → loans that pay interest

- Funds/ETFs → diversified baskets of assets

- Real estate → tangible property

Golden rules: Diversify to spread risk, be patient, and harness compound growth. Time in the market beats trying to time the market.

9. Value: Why Some Things Cost More

Value is subjective and perceived. A smartphone isn’t just plastic and glass—it delivers convenience, status, and utility, so people pay premium prices. Luxury brands or an iPhone command higher prices because of perceived desirability.

To build wealth, focus on creating value for others—through products, services, or skills that solve real problems or fulfill desires.

10. Time: Your Most Valuable (and Finite) Asset

Time is the one resource you can never get back. Most people trade it directly for money via jobs (one hour = one paycheck). The wealthy learn to leverage time through skills, systems, and—most importantly—compound interest.

Small, consistent investments made early can grow into life-changing sums over decades. Start now, stay consistent, and let time do the heavy lifting.

Final Thoughts: Take Control of Your Financial Future

These 10 concepts—taxes, banks, interest, inflation, recessions, credit scores, currency, investing, value, and time—form the foundation of smart money management. Mastering them reduces stress, prevents costly mistakes, and opens doors to financial freedom.

Start small today:

- Review your paycheck deductions

- Check your credit report

- Open a high-yield savings account or retirement plan

- Begin investing even $50 a month

Financial literacy is a superpower. As the video beautifully illustrates, understanding these basics turns money from a source of confusion into a tool for building the life you want.